High Interest Rates Have Not Slowed the Labour Market Sufficiently

The Canadian labour market has done it again, blowing past expectations for the fifth straight month. In April, a whopping 41,400 new jobs were added, more than double what economists predicted. Since February, monthly employment growth has averaged 33,000, following cumulative increases of 219,000 in December 2022 and January 2023.

The employment rate—the share of the population aged 15 and older—held steady at 62.4% for the third consecutive month in April. This is particularly noteworthy given the population grew by more than a million people in 2022 and is slated to snowball this year, thanks to immigration.

However, there is a catch. All the job growth in April was in part-time positions, while full-time jobs decreased by 6,200. But even with this slight hiccup, the labour market is still going strong, which means the Bank of Canada will likely continue its wait-and-see approach, even as we all wonder when the first rate cut will happen.

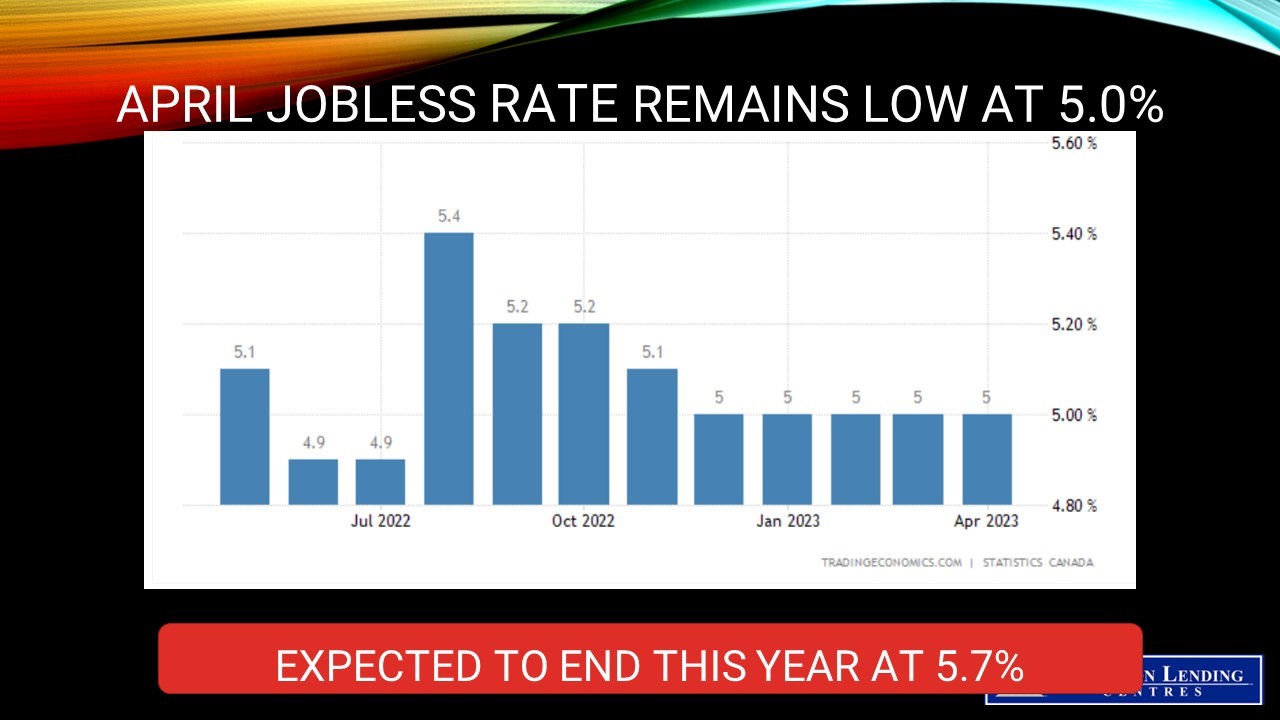

The jobless rate held steady at a near-record low of 5.0%, unchanged since December 2022. This remained near the record low of 4.9% observed in June and July 2022. Compared with April 2022, the unemployment rate was down 0.3 percentage points in April 2023.

Wage Inflation Remains High

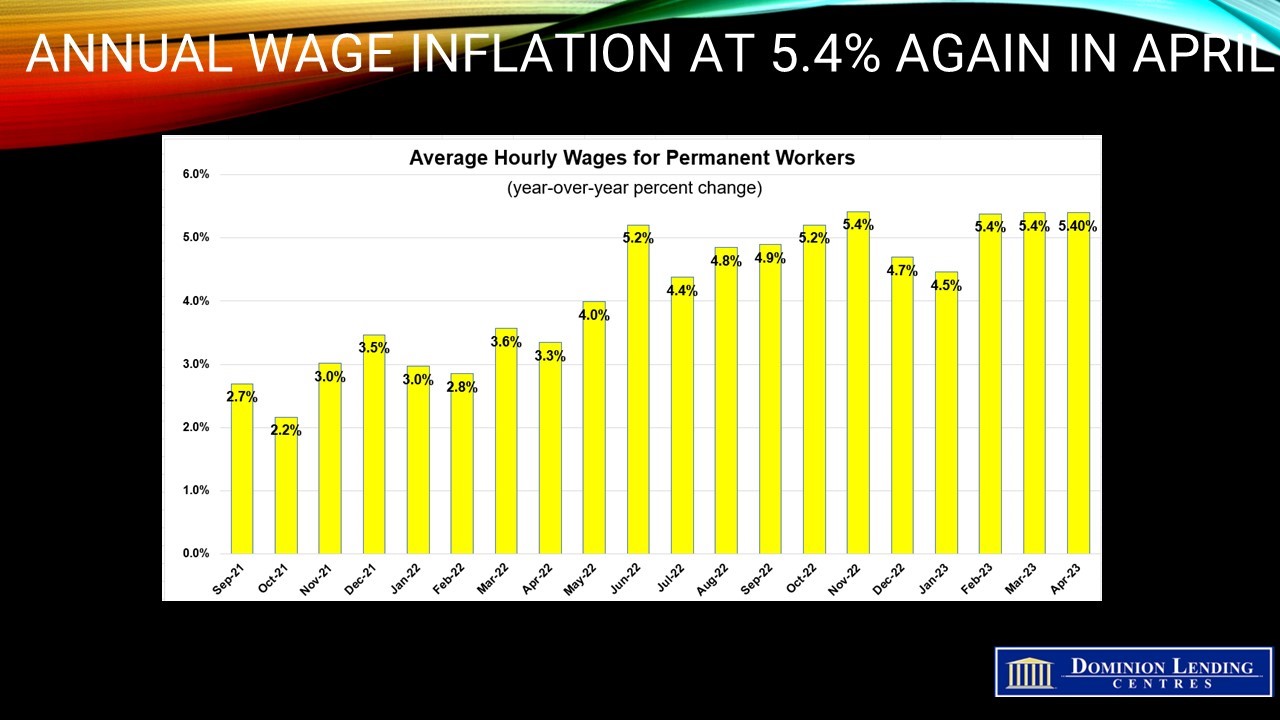

Of great concern to the Bank of Canada, average hourly wages rose by 5.2% on a yearly basis in a further sign of the labour market’s resilience, with wage growth now above the annual rate of inflation, which was 4.3% in March. It is not that wage inflation caused the surge in the Consumer Price Index last year, but continued vigorous wage hikes become impended in wage-price spiralling as higher costs give businesses cover to rate prices.

Bottom Line

The BoC, despite this report, isn’t likely to budge from its current policy stance. As more and more immigrants enter the workforce, the traditional markers of a strong jobs report are evolving. Even though the unemployment rate remains steady at 5%, it may indicate that we’ve hit a new equilibrium point. That’s why this seemingly “surprising” report doesn’t hold the same weight as it would have in the past.

In addition, the BoC can quickly point out the narrowness of sector hiring and the trend of full-time employment declining while part-time jobs rise. After today’s release, the BoC’s decision to stay on the sidelines is a wise move. But it also means that the Bank will not be in a hurry to cut rates this year

Vital Spring Housing Market Bodes Well For The Economy

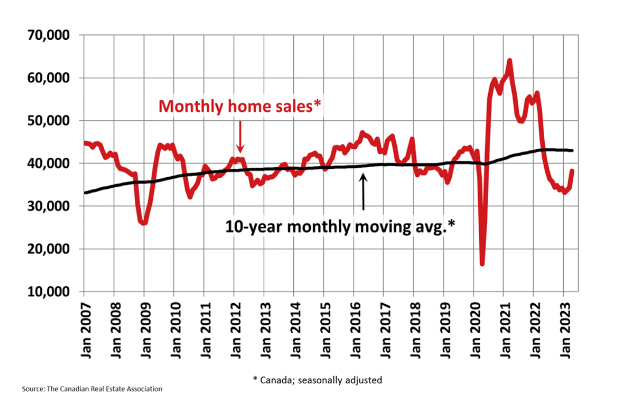

The Canadian Real Estate Association says home sales in April surged 11.3% month-over-month. The Spring rebound was on the heels of smaller back-to-back gains in the prior two months. Now that the Bank of Canada paused interest rate hikes and home prices in most regions have softened, homebuyers are scrambling for the minimal available housing supply.

Following the trend in recent months, the sales increase was broad-based but once again dominated by the B.C. Lower Mainland and the Greater Toronto Area (GTA). Toronto home sales, for example, rose by 27% m/m. That’s the most significant monthly increase over the past two decades, besides the rebound from the 2020 Covid lockdowns.

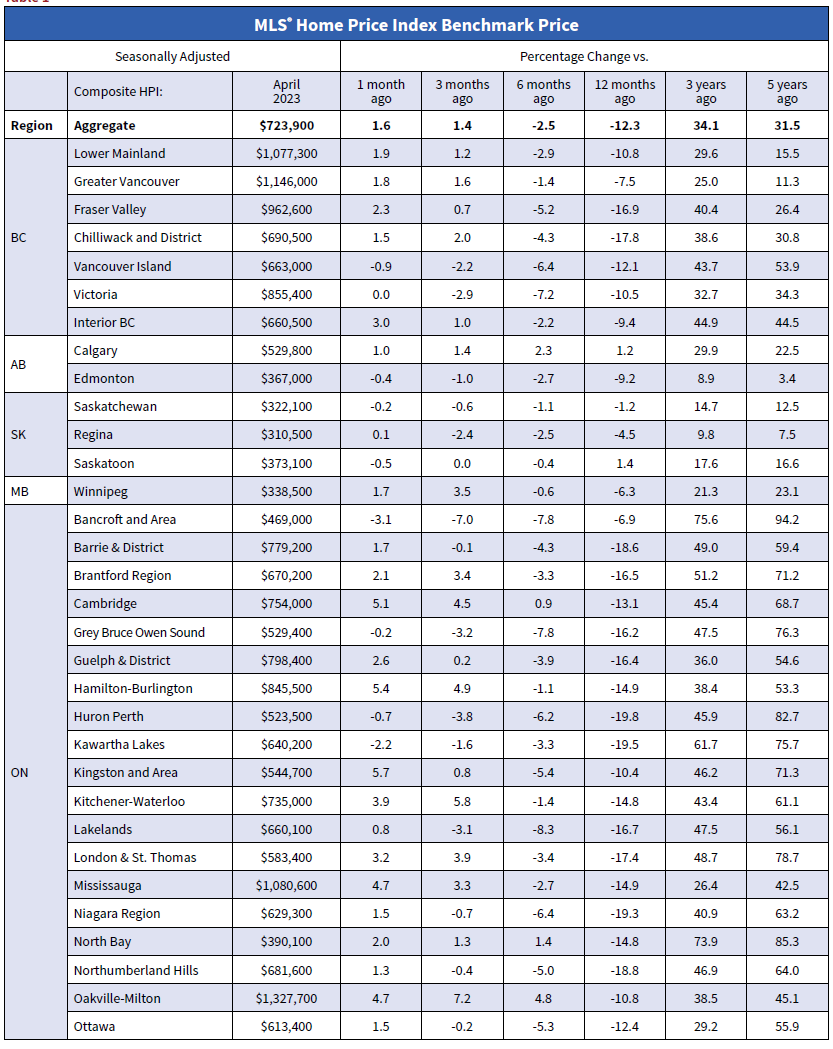

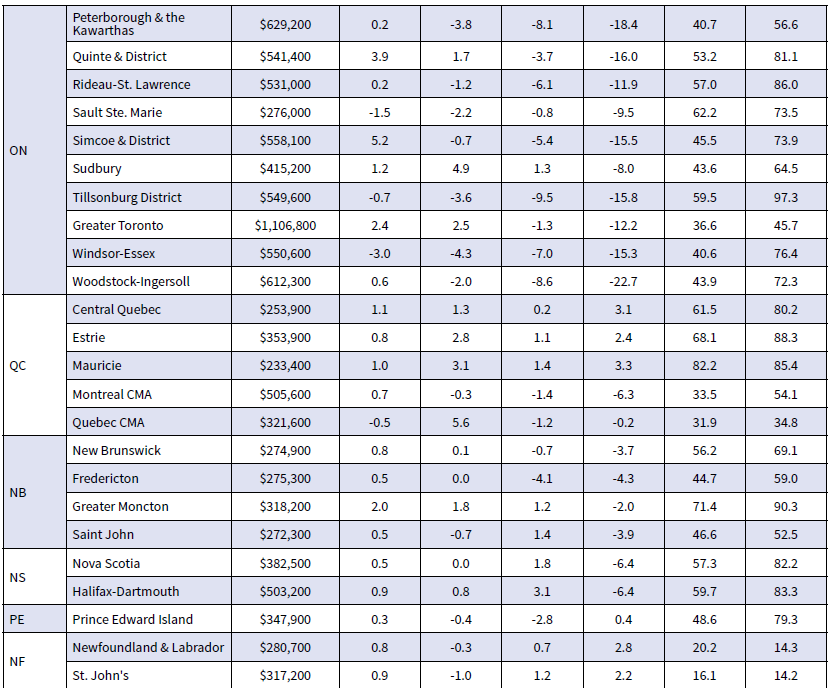

The benchmark price of a Toronto home rose 2.4% to C$1.11 million in April on a seasonally adjusted basis. The rise erased declines from earlier this year; prices are now up 0.5% year-to-date in the first four months of 2023.

New Listings

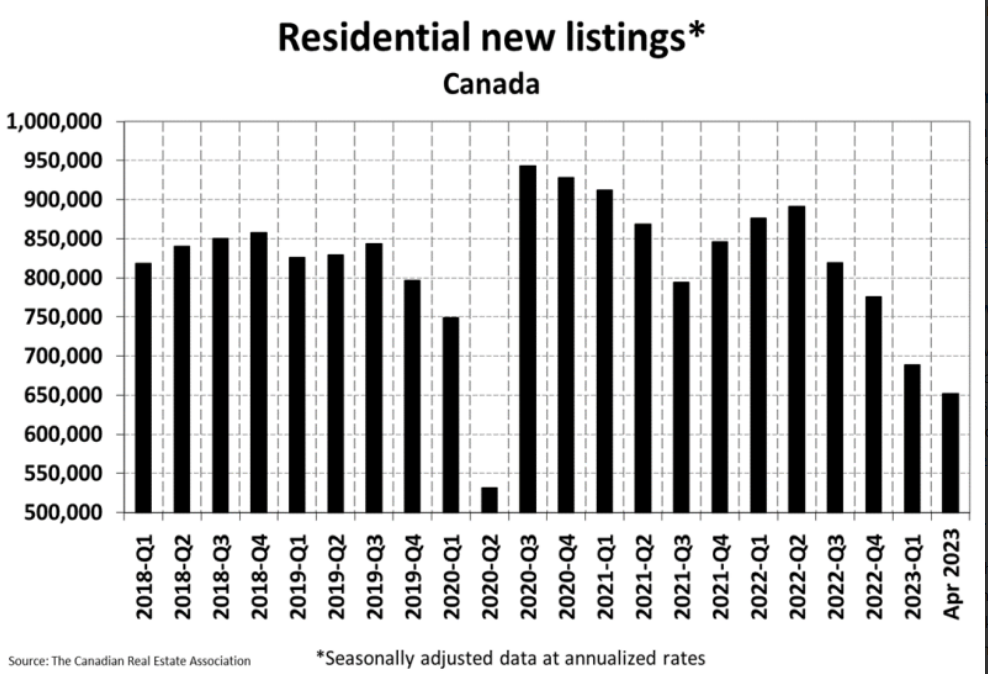

Housing inventory is not just low; it is extremely low, although more recent data suggest that new listings rose in the first week of May. The persistent lack of new listings is hurting home affordability.

The number of newly listed homes edged up 1.6% month-over-month in April; however, the bigger picture is that the new supply remains at a 20-year low. The number of new listings hitting the Toronto market trailed far behind the 27% increase in sales at just 2.8%. That helped shrink the supply of houses on the market, which had built up over the past year by 12.3% and left the city’s active-listings-to-sales ratio, a measure of how competitive the market is for buyers, tighter than the historical average.

And Toronto’s housing market isn’t the only one seeing tighter supply and rising prices. Vancouver, long one of the country’s most expensive markets, also saw its benchmark price rise 2.4% last month.

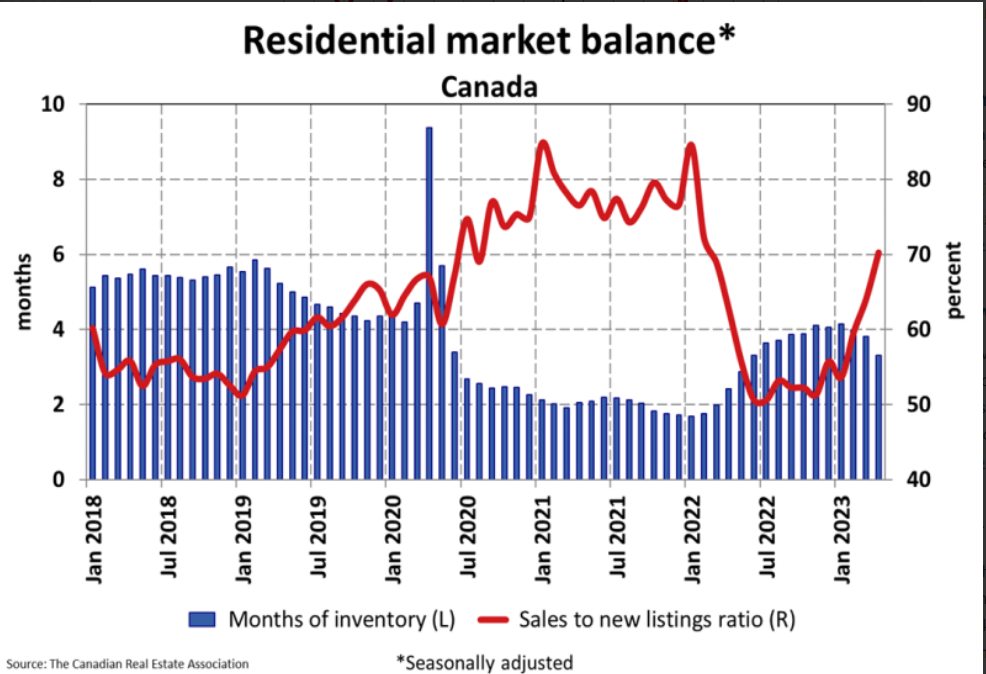

With national sales gains vastly outpacing new listings in April, the sales-to-new listings ratio jumped to 70.2%, up from 64.1% in March. The long-term average for this measure is 55.1%.

There were 3.3 months of inventory on a national basis at the end of April 2023, down half a month from 3.8 months at the end of March. The long-term average for this measure is about five months.

Home Prices

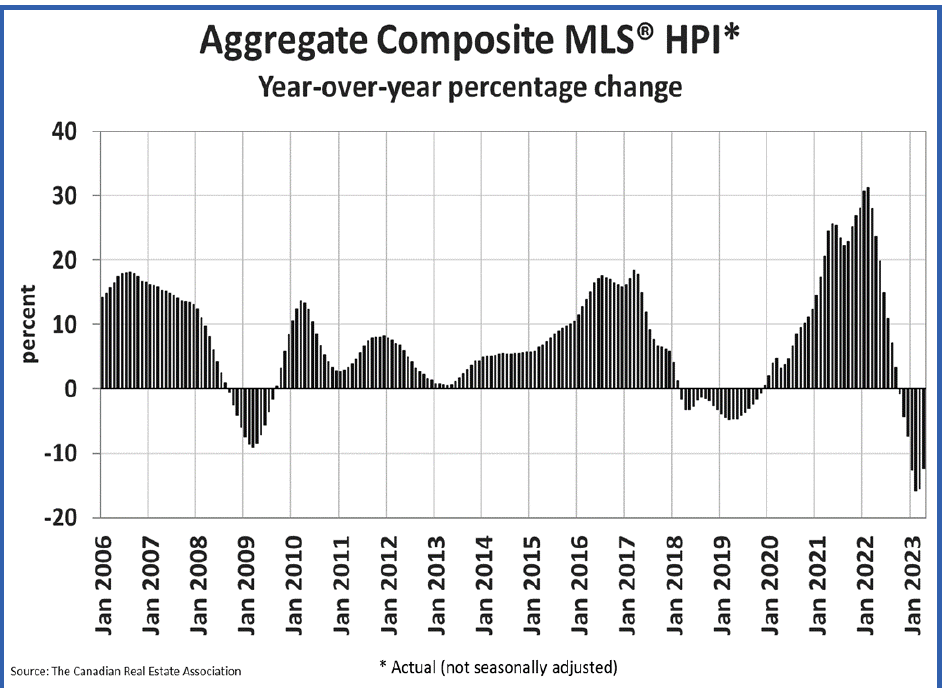

The Aggregate Composite MLS® Home Price Index (HPI) climbed 1.6% month-over-month in April 2023 – a significant increase for a single month. It was also broad-based. A monthly price rise from March to April was observed in most local markets.

The actual (not seasonally adjusted) national average home price was $716,000 in April 2023, down 3.9% from April 2022 but up $103,500 from January 2023, a gain owed to outsized sales rebounds in the GTA and B.C. Lower Mainland.

Bottom Line

A turnaround in the Canadian housing market is in train. While inventory remains extremely low, homes are not only selling but also selling fast. Short-term fixed-rate mortgages are popular with buyers. A significant change from before the Bank of Canada started raising rates.

While the Bank will likely hold rates steady for the remainder of this year, I do not expect Macklem to cut rates before then. All of this depends on inflation. We will get another read on inflation tomorrow.

The fact that labour markets are still strong and housing activity is picking up has got to make the Bank of Canada a wee bit nervous about inflation reaching the 2% target next year.

Another noticeable thing is the continued surge in the Canadian population, thanks to immigration, has worsened the housing shortage. The supply of new housing, especially affordable housing, is inadequate for the rapidly growing population. Moreover, a recent report by the C.D. Howe Institute’s Benjamin Dachis suggests there are major governmental impediments to providing adequate housing.

The Institute recommends:

- Enable the non-political enforcement of municipal housing policies

- Reform the fees on new development

- ease restrictions on building up and out